How the trail forms

Follow ordinary public records, forms, profiles, app signals, broker feeds, and breaches as separate sources that can be linked into one profile.

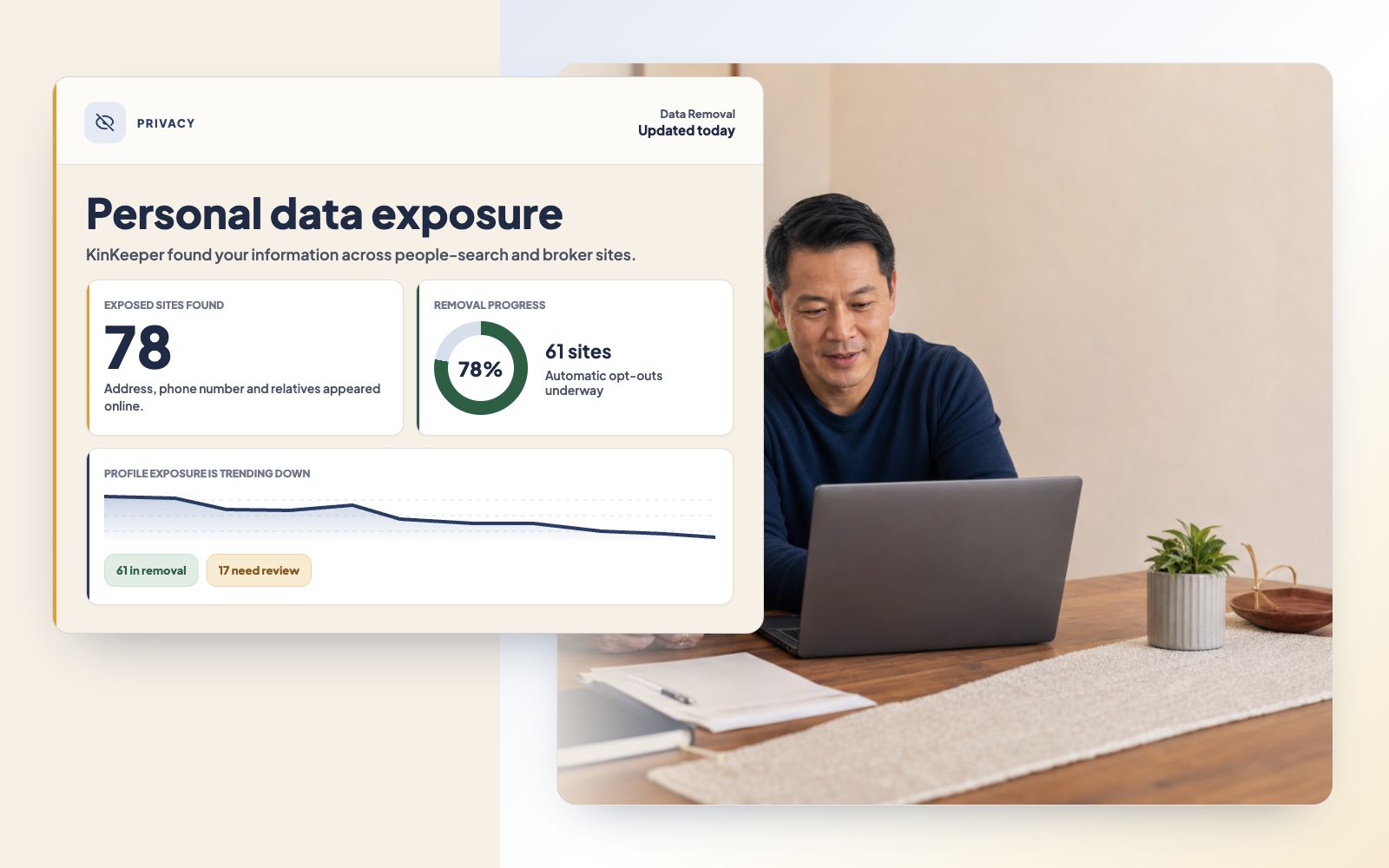

KinKeeper research

Personal data does not cause fraud, but it can make someone easier to locate, classify, and approach. This evidence review explains how ordinary records become targeting intelligence, what privacy cleanup and account security can accomplish, and what remains unproven.

Free online report and PDF. No email required.

Read online · PDF available

Read online · PDF available What the evidence says

People-search sites can combine names, ages, addresses, property history, and family relationships. Commercial data can add purchasing behavior, interests, inferred traits, and response patterns. The practical response is layered: reduce high-value public exposure, stop unnecessary new sharing, and harden important accounts.

Follow ordinary public records, forms, profiles, app signals, broker feeds, and breaches as separate sources that can be linked into one profile.

See why an opt-out can remove a current listing from one route without erasing public records, every downstream copy, or future reappearance.

Keep the effect of broker removal on scam attempts, completed fraud, and financial loss separate from the exposure that can be observed.

A practical framework

Find the public combinations that join a contact route with age, home, property, relatives, or other useful context.

Remove high-priority listings, tighten public family details, separate contact routes, and stop unnecessary sharing.

Strengthen important accounts, save recovery routes and confirmations, and use a light recheck schedule.

Complete online edition

The complete research, methodology, limitations, and source ledger are published below as readable, searchable HTML.

Prefer the PDF? Open it herePersonal data does not cause fraud. It can, however, make a person easier to locate, classify, and approach. People-search sites can turn one identifier into a report containing age, addresses, property history, and family relationships. Commercial brokers can add purchasing behavior, interests, inferred traits, and response patterns.12

This is not only a theoretical privacy problem. In the Epsilon criminal case, federal prosecutors showed that employees used models built on a database of 100 million U.S. households to identify likely responders and knowingly sold targeted lists to fraud operators. One client used those lists in a scheme that defrauded more than 218,000 people of more than $23.7 million.323

Privacy cleanup is best understood as exposure reduction, not a force field. It gives unknown senders less accessible information while account security and independent verification protect against different failure points.

The practical response is layered. Remove high-value public listings, stop providing primary contact information to low-trust forms, strengthen critical accounts, and keep a consent-based family review routine. These steps reduce particular exposures. Research has not yet quantified how much broker removal changes scam attempts or financial loss.

| What the evidence supports | Finding |

|---|---|

| Direct evidence | Modeled consumer lists have been knowingly sold to operators of elder-fraud schemes. |

| Defensible action | Current listings can be removed, important accounts hardened, and future sharing reduced. |

| Open question | The effect of broker removal on fraud incidence and loss has not been adequately measured. |

Privacy conversations often jump from “this information is available” to “removing it prevents fraud.” The first statement is observable. The second requires outcome evidence the field does not yet have. This report uses three evidence grades so practical guidance does not borrow more certainty than the research can support.

Fraud reports establish urgency, not the effectiveness of any privacy intervention. FTC reporting shows $2.4 billion in reported 2024 losses among older adults, about four times the amount reported in 2020. Reports of imposter-scam losses above $100,000 rose nearly sevenfold over the same broad period.911 Complaint data undercount harm and should not be treated as a full prevalence estimate.

The raw material is often mundane: a deed, shopping form, donation, app permission, public post, or old breach. The power comes from linkage, inference, and reuse.124

Not all data brokers do the same job. Some support marketing, fraud prevention, identity verification, analytics, or public-record search. Risk depends on the information, buyer, purpose, safeguards, and ability to correct or delete it.

A phone number is useful for contact. A phone number linked to age, address, family, property, interests, and past responses can support a much more specific approach. The system value comes from combining and updating fragments.

| Stage | What happens |

|---|---|

| Collect | Records and signals enter public, commercial, device, or criminal datasets. |

| Link | Names, addresses, phones, emails, devices, and household members are matched. |

| Infer | Models assign likely interests, traits, needs, value, or response behavior. |

| Segment | People are grouped for marketing, risk, eligibility, research, or targeting. |

| Reach | A message, call, ad, letter, or account attempt uses the selected route. |

Three distinctions prevent bad conclusions:

A household cannot control every upstream record. It can reduce the easiest public combinations, limit future sharing, and harden the accounts that turn information into access.

According to the Justice Department, Epsilon used transactional data and algorithms to predict “responsive buyers” across a database of 100 million U.S. households. Employees knowingly sold targeted lists to operators sending deceptive sweepstakes and astrology mailings, particularly affecting older and vulnerable people.323

| Documented measure | Result |

|---|---|

| Households in the modeling database | 100 million |

| Victims in one client’s scheme | More than 218,000 |

| Loss associated with that scheme | More than $23.7 million |

The case establishes that targeting data and response modeling can materially facilitate fraud operations. It also shows how legitimate customer, nonprofit, and charitable relationships can feed data later misused by bad actors. DOJ reported that more than 12,000 victims in one scheme were defrauded more than 20 times.323

The case does not establish that every broker or marketing use is fraudulent, that a particular opt-out would have prevented the scheme, or that the same mechanism explains every phone, text, social, or account-takeover scam.

Older adults report losing money to fraud at a lower rate than younger adults in FTC complaint data, yet report much higher median losses when a loss occurs and are overrepresented in several high-loss scam categories. Age should not be used as a shortcut for incapacity.9

The relevant differences are the information and stakes:

The task is to redesign exposure and verification around real conditions, not to ask whether an older adult is “good with technology.” Privacy support should reduce chores while keeping choices and account ownership with the person at the center.

For a family member or trusted person:

The FBI describes generative AI being used to produce believable text, fake profiles and identification, synthetic images, cloned audio, and deceptive video. When a sender already has names, relationships, institutions, interests, or recent events, those tools can make personalization faster and more polished.10

| What AI changes | What still has to happen |

|---|---|

| More fluent drafting in many tones and languages | A channel still has to reach the person. |

| Faster synthesis of fragments into a plausible story | The sender must keep the person inside the attacker’s channel. |

| Cheaper images, profiles, audio, and video | The person must disclose, install, authenticate, transfer, or pay. |

| More variants and follow-up at lower production cost | Independent verification can still break the narrative. |

Reducing raw material can help upstream. Independent verification and strong authentication remain necessary downstream because convincing stories can be created from information that cannot be removed.

Older adults already use AI, voice assistants, home security, health tools, and connected services to support independence. The right question is not whether to reject technology. It is what the tool collects, who can access it, what is retained, and whether the benefit is worth the exposure.12131419

Before connecting a tool, ask:

A University of Michigan poll found that 55% of adults age 50-97 had used conversational AI and 92% wanted to know when information was AI-generated. An AARP survey found 69% of adults age 50+ were uncomfortable sharing personal health information with an AI health tool.1319 These figures come from different surveys and should not be combined.

Deletion, minimization, contact-route separation, and account security act at different points. The strongest plan layers them instead of treating one product or setting as the solution.

The FTC explains that people-search sites generally offer free opt-outs. A successful request can stop the site from selling its current listing, but information may remain in public records, appear inside a relative’s report, or return when new data arrives.1

| Removal can | Removal cannot establish |

|---|---|

| Remove a current profile or matching record from a participating site. | That public records or every downstream copy were deleted. |

| Reduce an easy public combination of contact, age, address, property, and relatives. | That a phone number, email, or identity detail is absent from breaches. |

| Create a documented request and reason to recheck later. | That future records will never recreate a profile. |

| Automate repeated requests and monitoring when a service covers the relevant brokers. | That removal caused fewer scam attempts, completed frauds, or losses. |

A 2025 preprint tested compliance across 543 registered California data brokers and identified request and verification problems. It helps explain implementation friction; it does not measure fraud outcomes and had not completed peer review by this report’s evidence cutoff.17

California residents can submit one request through the Delete Request and Opt-out Platform to more than 600 registered data brokers. Consumer requests opened in January 2026. Beginning August 1, 2026, brokers must process requests on a recurring cycle and report status. The system does not apply to every company or record.56

A careful explanation includes four limits:

DROP is a concrete 2026 example of a broader shift from hundreds of individual opt-outs toward persistent, centralized deletion instructions.

Removal addresses information already held. Data minimization addresses what is supplied next. The goal is not withdrawal from digital life; it is to stop using high-value contact and identity details where they are unnecessary.

Use the minimum information needed for the transaction, and keep primary family and account routes out of low-trust forms.

Removing a people-search listing does not invalidate a stolen password. Strong authentication does not remove a home address. Households need both exposure reduction and access control.

NIST treats cryptographic authentication as phishing-resistant because a secret is not manually entered into an impostor site. In 2025 workshops, older adults liked the reduced memory burden of passkeys but wanted support for setup, transfer, device loss, and shared-device concerns.1618

A privacy plan should end with fewer chores, not a second job. This framework prioritizes the information most useful for reach and credibility, then adds account controls and a light maintenance rhythm. It can be used by an older adult alone or with a trusted person.

Search a name, phone, email, and address safely. Record the profiles that combine contact information with age, property, or relatives. Choose the one listing that reveals the most useful bundle.

Complete high-priority opt-outs, tighten public family details, separate contact routes, and remove unnecessary app permissions. Finish one real removal or save its exact next action.

Harden primary email and financial accounts, save official routes, document recovery, and schedule a light recheck. Set a 30-day follow-up and quarterly review.

Do the highest-value work first. A household does not need perfect invisibility; it needs less easy exposure, stronger access controls, and a reliable way to verify surprises.

The person at the center should know what is being searched, removed, shared, and monitored. Families, institutions, and technology providers can reduce repetitive work without converting support into surveillance.

Measures worth publishing include:

“Removed from 60 broker sites” is a removal result. It is not proof of fewer scams or lower loss unless those outcomes were separately measured.

KinKeeper’s free Personal Data & Privacy Playbook follows the same See, Shrink, Steady structure. It helps an older adult or trusted person complete or prepare one removal, strengthen or prepare one important-account action, and save a lightweight maintenance plan.

KinKeeper’s free data-broker opt-out guides support do-it-yourself removal. Families who do not want to repeat every request by hand can also consider privacy tools that combine exposure scanning with recurring automated removal, including KinKeeper Privacy.

Availability as of July 15, 2026: KinKeeper Data Removal is rolling out. The public Exposure Scan is pre-launch.2122

The next scheduled review is October 15, 2026, or earlier if DROP implementation, federal data-broker policy, major enforcement, outcome research, or KinKeeper Privacy availability materially changes.

Companion Playbook

The free Personal Data & Privacy Playbook helps an older adult or trusted helper run a safe exposure check, complete or prepare one removal, strengthen an important account, and save a manageable maintenance plan.

Keep going