What the evidence measures

Keep reported complaints, reported losses, suspicious activity, and population-level credit research in their proper lanes.

KinKeeper research

The strongest warning sign is rarely one unusual purchase. It is a meaningful change from a person's own financial baseline, especially when several signals appear together. This research review explains what transactions and property records can reveal, what they cannot establish, and how families can check a concern without taking over.

Free online report and PDF. No email required.

Read online · PDF available

Read online · PDF available What the evidence says

A new purchase can be planned. A missed bill can have a simple explanation. The useful signal is often the change around an event: a new recipient, unfamiliar payment route, repetition, missing income, or another related change. The right response starts with context and official verification.

Keep reported complaints, reported losses, suspicious activity, and population-level credit research in their proper lanes.

Compare a new event with the person's own baseline, then look for repetition, sequence, missing events, and corroboration.

Use owner-controlled alerts, limited trusted-contact roles, and official verification routes that preserve the older adult's choices.

A practical framework

Define what is normal and what the account owner wants watched.

Describe meaningful changes without turning an alert into a diagnosis or accusation.

Pause, ask, and verify through an official route before more money moves.

Complete online edition

The complete research, methodology, limitations, and source ledger are published below as readable, searchable HTML.

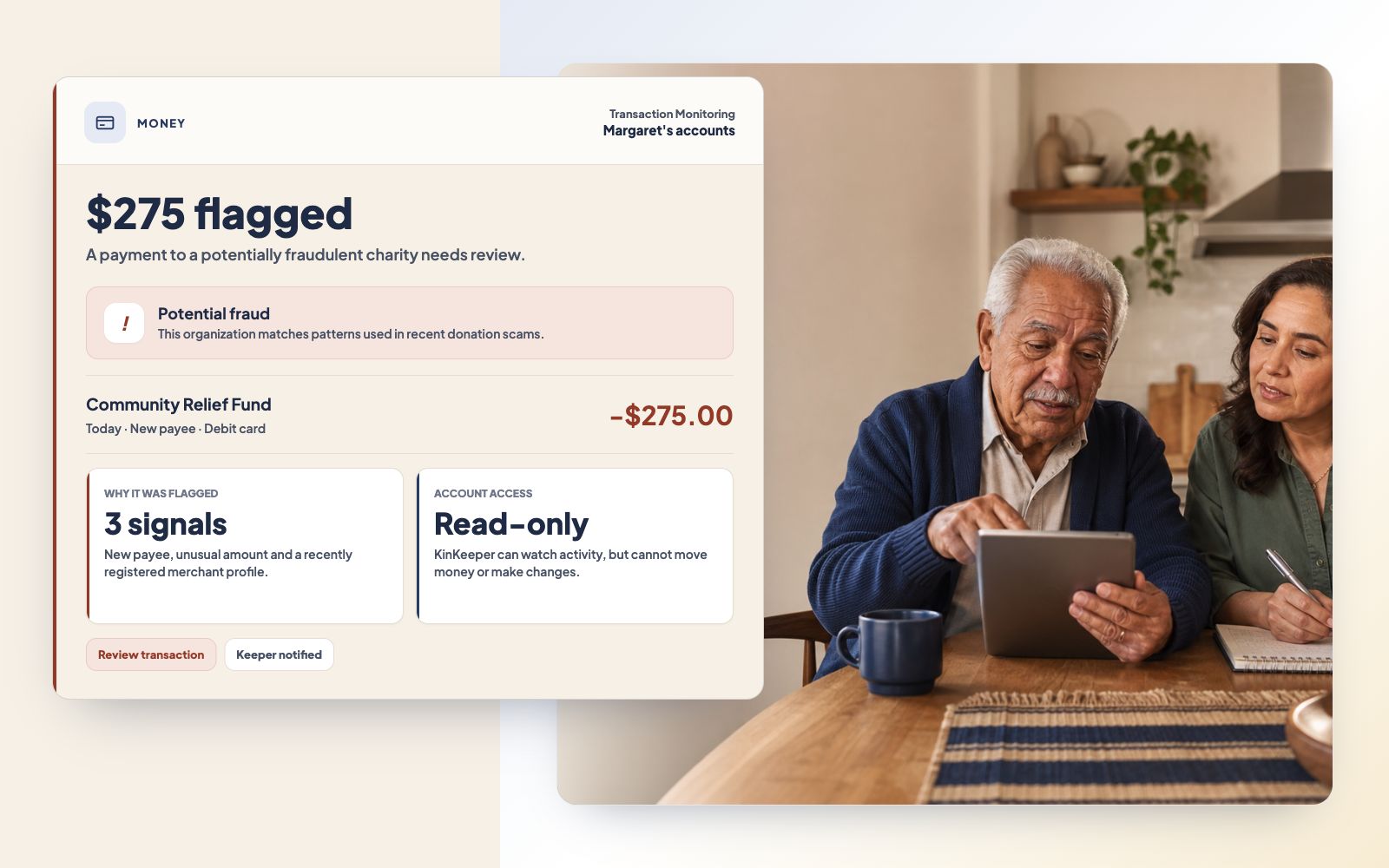

Prefer the PDF? Open it hereA $900 transfer can be ordinary for one household and unprecedented for another. A new charity may reflect a deliberate gift. A missed utility payment may be a bank error, a move, a changed due date, a cash-flow problem, or a sign that managing bills has become harder. The transaction alone does not settle the question.

What deserves attention is often the change around it: a new recipient, an unfamiliar payment route, several transfers in quick succession, money moved from savings immediately before it leaves the account, an expected deposit that does not arrive, or an abrupt change in who controls statements and access. Federal guidance repeatedly treats activity that is unusual for the particular account holder as more informative than a universal rule about what an older person should buy.78

The useful question is not, “Was that a bad purchase?” It is, “What changed, what else changed with it, and is there a safe explanation?”

That approach protects two things at once. It gives families and institutions a better chance of recognizing fraud or exploitation, and it protects the older adult from having ordinary choices treated as evidence of incapacity.

| Measure | Result | What it means |

|---|---|---|

| IC3 complaints from people age 60+ in 2025 | 201,266 | Reports submitted to one federal cybercrime complaint system |

| Reported IC3 losses for people age 60+ in 2025 | $7.748 billion | Reported loss, not a national prevalence estimate |

| IC3 complainants age 60+ reporting losses above $100,000 | 12,444 | High-loss reports within the IC3 dataset |

| FinCEN elder-financial-exploitation-related filings analyzed | 155,415 | Suspicious activity reports from financial institutions |

| Dollar value indicated in those FinCEN filings | About $27 billion | Suspicious activity, not verified victim loss |

Sources: FBI IC3 2025 Annual Report and FinCEN’s 2024 trend analysis.12

This report examines financial changes involving community-dwelling older adults and the people or institutions helping them. It focuses on everyday transaction activity, credit-management research, trusted contacts, known-person exploitation, and property-record monitoring. It does not evaluate investment suitability, diagnose a health condition, or provide legal advice.

Four categories can produce similar-looking account activity:

The categories can overlap. A scammer may gain remote access and take over an account. A trusted person may conceal withdrawals. A household may experience a genuine money-management problem and then become more vulnerable to a scam. The same visible signal can therefore require different responses.

A financial baseline is a working picture of what is typical for the person and account. It can include:

A baseline is not a rule that freezes someone into past behavior. People change their minds and routines. It is a comparison point that makes a new event easier to explain.

KinKeeper conducted a narrative synthesis of sources available through July 16, 2026. Priority went to current federal regulators and law-enforcement reports, official consumer guidance, and peer-reviewed original research. Historical sources were used when they supplied a method or detail not available in newer reporting.

The synthesis keeps three evidence streams separate:

This is not a systematic review or meta-analysis. It does not estimate the sensitivity or specificity of consumer transaction-monitoring products, because the necessary independent outcome evidence is not yet available.

The FBI’s 2025 annual report recorded 201,266 complaints from people age 60 and older, 37% more than in 2024. Reported losses reached $7.748 billion, a 59% increase. The report also recorded an average reported loss of $38,500 and 12,444 complainants reporting losses above $100,000.1

Investment fraud accounted for the largest reported loss among people age 60 and older in that dataset, followed by tech-support scams, confidence or romance fraud, business email compromise, and government impersonation. Cryptocurrency appeared as a descriptor in $4.347 billion of reported losses for that age group. A descriptor can overlap with a crime category, so these values are not separate buckets to add together.1

FTC data tell a complementary story. Adults age 60 and older reported $2.4 billion in fraud losses to the Consumer Sentinel Network in 2024, roughly four times the amount reported in 2020. Older adults continued to report losing money at a lower rate than younger adults, but reported much higher median losses when a loss occurred. That distinction matters: the risk is not that older adults uniformly make poorer decisions. It is that some successful schemes produce unusually severe losses.3

In high-loss business and government impersonation reports, the FTC found that reports of losses above $10,000 more than quadrupled from 2020 to 2024, while reports above $100,000 rose nearly sevenfold. For losses above $100,000, bank transfers were the most frequently reported payment method. The starting story often involved a fake security alert, business, or government agency telling the person that money was at risk.17

FinCEN examined 155,415 Bank Secrecy Act filings submitted between June 15, 2022 and June 15, 2023. The filings indicated roughly $27 billion in elder-financial-exploitation-related suspicious activity. About 80% involved scams, usually money transferred to a stranger or imposter for a benefit that never arrived. About 20% involved theft by a person who was otherwise trusted.2

The distinction changes what monitoring must notice. Stranger scams often produce a visible payment event: a wire, crypto purchase, transfer app, cashier’s check, gift card, or rapid movement of funds. Known-person exploitation may look quieter: recurring ATM withdrawals, card use by another person, changed account ownership, missing statements, transfers to a relative, misuse of a power of attorney, or an unexpected deed change.81215

No transaction engine can observe coercion, fear, isolation, or who is standing beside the account holder. That is why financial data should support, not replace, a human conversation.

Paying bills on time requires attention, memory, planning, arithmetic, judgment, and the ability to manage changing instructions. A difficulty in any one part of that process can appear in the financial record before it appears in a clinical record. It can also arise for reasons unrelated to cognitive decline, including illness, grief, depression, vision changes, technology changes, income pressure, or a simple administrative error.

The relevant research asks a narrow question: when a large group of people later receive a memory-disorder diagnosis, do their earlier credit outcomes differ from otherwise comparable people who do not receive that diagnosis?

Gresenz and colleagues linked nationally representative credit-reporting data with Medicare records. The research followed nearly 2.5 million older adults over 17 years, including approximately 500,000 who were later diagnosed with Alzheimer’s disease or a related dementia. The peer-reviewed paper reported effects years before diagnosis across payment delinquency, delinquent balances, credit utilization, mortgage outcomes, and credit scores.45

NIA’s summary reported that missed credit-card payments began increasing about five years before diagnosis and mortgage-payment problems about three years before diagnosis. In the year before diagnosis, people in the later-diagnosed group were more than 34% more likely to miss a credit-card payment and 17% more likely to miss a mortgage payment than in earlier years.4

The effects were not uniform. They were larger for single people and Black individuals in parts of the analysis. That pattern may reflect differences in household support, resources, credit access, structural inequality, and timing of diagnosis as well as disease effects. It is a warning against building a single “normal” model for every household.45

An earlier JAMA Internal Medicine study also found small but statistically significant differences before diagnosis. Single Medicare beneficiaries later diagnosed with Alzheimer’s disease or a related dementia were more likely to miss payments as early as six years before diagnosis and to develop subprime credit scores about two and a half years before diagnosis than demographically similar beneficiaries without the diagnosis.6

The research does not show that a late bill proves cognitive decline. It does not validate a clinical score from a checking account. It does not show that family access to every transaction improves health or financial outcomes. The studies rely primarily on credit-report events, which omit cash spending, many bank-account transactions, fraud that is not reported to a lender, informal household arrangements, and the explanation behind the event.456

The appropriate inference is narrower:

A new, repeated difficulty managing bills can be worth discussing, especially when it appears alongside other changes. It is not a diagnosis and should not be used to remove a person’s control.

If financial changes arrive with new memory concerns, confusion, difficulty completing familiar tasks, or another health change, the older adult can decide whether to discuss the pattern with a qualified clinician. A monitoring product should not make that referral automatically from transaction data alone.

Four questions make an alert more useful and less intrusive.

The fourth question is where a pattern often becomes meaningful. A new payee alone may be routine. A new payee followed by repeated P2P transfers, a savings-to-checking transfer, and a rapid balance decline deserves a faster review. A missed pension deposit may be a processing delay. A missed deposit followed by overdraft fees and unpaid recurring bills shows a broader problem.

| Signal | Alone | Stronger when combined with |

|---|---|---|

| First payment to a new recipient | Often ordinary | Large amount, repeated transfers, risky rail, secrecy or urgency |

| Wire, crypto, gift card, or P2P payment | Legitimate uses exist | New recipient, unusual amount, rapid repetition, account drain |

| Large purchase | May be planned | New merchant, out-of-pattern channel, unusual location, follow-on transfers |

| Missed expected bill | Could be an administrative error | Repetition, late fees, service interruption, other missed bills |

| Missing expected deposit | Could be timing or eligibility | Low balance, overdraft, changed deposit destination, repeated absence |

| Frequent ATM withdrawals | May reflect a new cash preference | Larger amounts, new locations, an accompanying person controlling access |

| Dormant account becomes active | Could be planned consolidation | New payee, rapid withdrawal, changed contact information |

| Property-record change | Could be authorized | Owner does not recognize it, unexpected loan contact, identity-theft indicators |

Regulators give financial institutions similar examples. An unexpected large wire from an account with no comparable history is a reason to investigate, not because every wire is fraudulent, but because the account’s own history makes the event unusual.7

Some payment routes deserve faster review because money can move quickly or recovery can be difficult. Current complaint data repeatedly identify bank transfers, cryptocurrency, cash, payment apps, gift cards, and wires in high-loss scams.1317

Useful signals include:

The response should not be “crypto equals fraud” or “a new payee is prohibited.” It should be “this route and sequence are unusual; verify before more money moves.”

Not every harmful pattern arrives as a dramatic transfer. A useful monitoring plan also looks for money that leaves gradually or fails to arrive:

These events are not necessarily exploitation. They may reveal a merchant issue, a benefit problem, a forgotten renewal, a cash-flow strain, or a task that has become harder to manage. The value is the earlier conversation.

Transaction data become especially limited when the concern involves someone the account holder knows. CFPB and DOJ guidance identify signs that may never appear in a merchant category:

Families should be careful here. The person receiving an alert may also be the person misusing the money. Monitoring design therefore needs more than “notify the family.” It needs owner-controlled routing, the ability to choose more than one trusted channel, and a clear path to the financial institution or an outside professional.

Property can be the household’s largest asset, yet it sits outside ordinary bank alerts. A property-monitoring service may compare current public records with a confirmed baseline and flag a change in ownership, deed, lien, mortgage, or related record when the available source changes.

That can be useful. It does not create a lock around the title. The FTC warns that services marketed as “home title locks” do not stop a fraudulent filing and are not title insurance. At most, monitoring may tell the owner after a record has changed.13

A responsible property alert should therefore say:

It should not say that the home was “stolen,” that fraud was confirmed, or that monitoring prevented a transfer.

A property-record change becomes more concerning when it appears with an unexplained loan, large deposit followed by rapid withdrawals, a new person controlling mail, or identity-theft indicators. The combination can guide a faster review. It still cannot establish who authorized the filing or whether the legal record is valid.

Brokerage firms ask customers to consider naming a trusted contact. That person is similar to an emergency contact: the firm may reach them when it cannot contact the account owner or reasonably suspects exploitation. The trusted contact does not automatically gain authority to trade, make decisions, or view balances and transactions. Those powers require separate legal authorization.1016

This limited role is a good model for family monitoring. The account owner can choose:

The goal is not to give a family member a continuous view of someone’s spending. It is to create a second channel for events the owner has decided deserve help.

An alert should open with observable facts:

“This transfer is new and larger than your usual transfers. Did you mean to send it?”

It should not open with an accusation:

“You are making bad decisions again.”

The first version invites context. The second creates shame, encourages secrecy, and turns the family relationship into a test of capacity.

Helpful family language includes:

A useful alert answers five questions:

A score without those facts can create false confidence or unnecessary alarm. The account owner and trusted person need the evidence, not a machine’s verdict.

Ongoing monitoring creates value even when nothing is flagged, but only if the user can see what was reviewed. A clear status can show:

“No change found” is different from “no current data.” A monitoring product should never blur the two.

The cognitive research supports education and careful planning. It does not support a consumer product declaring that someone has cognitive decline based on a transaction pattern. A responsible system may flag repeated missed payments, unusual fees, or a broad pattern break. It should describe those events in financial terms and leave health interpretation to the person and a qualified clinician.45

When an event may still be in progress:

If the concern involves a brokerage account, the firm may have trusted-contact and temporary-hold procedures. If the concern involves property, contact the official recorder or land-record office and a qualified attorney or title professional appropriate to the situation.716

No response path guarantees recovery. Speed can preserve more options, especially before money moves through additional accounts.

List the accounts, expected deposits, recurring bills, ordinary transfer routes, important property records, and official contact methods that matter. The account owner decides what is included and who may help.

Look for a change in amount, recipient, route, timing, frequency, location, account activity, expected income, bill payment, access, ownership, or property record. One signal is a question. Several related signals can create urgency.

Leave the channel that produced the request or alert. Confirm with the account owner and the institution through an official route. Bring in the trusted person the account owner selected, not the person who simply demands access.

This framework does not require a household to monitor every purchase. It creates a repeatable response for the moments already defined as important.

The companion Money Safety & Monitoring Playbook helps an older adult or family:

The Playbook is practical and can be completed without connecting financial accounts. The research paper explains why those actions matter and where the evidence remains uncertain.

KinKeeper Money Monitoring is designed to provide a second set of eyes across read-only financial activity and selected property records. It can compare current activity with a household’s established patterns, explain why an event deserves attention, and route masked alerts according to the account owner’s choices. KinKeeper cannot move money, determine whether someone has cognitive impairment, prevent a fraudulent property filing, or guarantee that a loss will be avoided.18

The product is one optional way to maintain the review routine described in this paper. A household can also use bank alerts, brokerage trusted contacts, official county record alerts, calendar reminders, and a written family plan.

This report has several limits.

The most important research gaps are product-level outcomes, false-positive burden, autonomy and privacy effects, performance across diverse households, and the ethics of using financial data for health-related inference.

Evidence reviewed through July 16, 2026. Next scheduled review: October 16, 2026, or earlier if major fraud reporting, financial-regulatory guidance, cognitive research, or KinKeeper product availability changes.

Companion Playbook

The free Money Safety & Monitoring Playbook helps older adults and trusted helpers define a useful baseline, choose sharing boundaries, practice proportionate responses, and save a one-page household plan.

Keep going